European market continues recovering from crisis. The greatest growth of car sales by the end of 2014 has been observed in Spain by 18.4% (0,89 mln cars). Next, if consider the key European markets, comes UK: + 9,3% (2.5 million cars), Italy: +4,2% (1.4 million cars), Germany:+2.9% (3.0 million cars) and France: +0.3 % (1.8 million cars). In Russia there is a negative trend -10,2% by the end of 2014 (2.3 million sold cars).

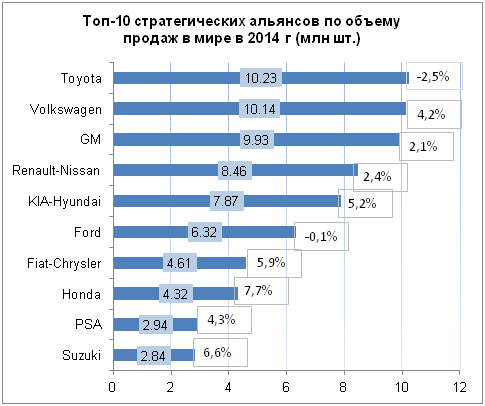

Despite the slowdown in market growth, most global key alliances of car manufacturers continue finding ways to increase their sales.

In 2014 PSA/Peugeot-Citroen also announced its intention to sell or close a number of German outlets to increase the profitability of the rest network. In July, Daimler reached an agreement to sell 213 Mercedes-Benz dealerships that it owned in Germany.

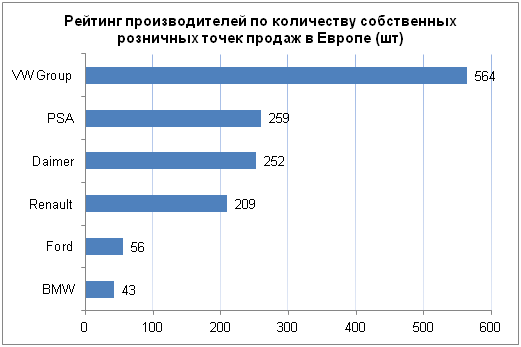

Number of dealerships, company-owned and independent declined in Western Europe by 12% since 2007 (up to 47500 units). The sharpest reduction was in Spain (24%), followed by Italy (15%). BMW and VW Group, which reduced their dealer networks by 13% and 9% respectively, made significant progress and have arguably the best dealer network in Europe, according to the Bernstein Research report.

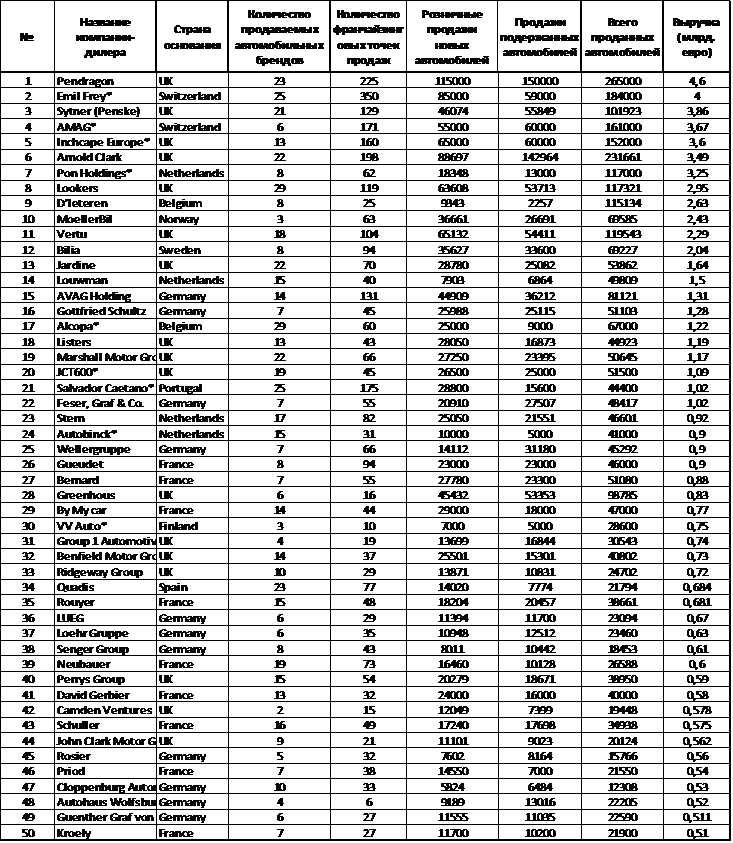

Table 1. The largest independent dealer groups in Europe

In a situation of European and US developed markets saturation automakers and dealer groups have started to rebuild and to strengthen dealer networks by implementing new processes and standards. According to McKinsey Company, efforts were directed to carefully monitor of such indicators as conversion metrics through the sales funnel or average discount per car to reveal lagging brands and actively manage dealer’s performance.

Car manufacturers constantly improve requirements regarding compliance with corporate standards, imposing additional conditions, which may include mono-brand restrictions, organizational and financial separation between the dealers of new and used vehicles, minimal marketing budgets, etc. According to it, more and more manufacturers adject additional conditions in dealer contracts, creating online channels that complement traditional dealer channels, as well as increase control over appearance and operations of the dealer network.

Unlike many other industries, such as electronics and appliances, where importance of dealership is decreasing, car dealer salons remain a key factor of interaction with customers for three reasons: 1) most customers still want to test the car before buying, because buying a car is a major investment; 2) customers often want to get an expert advice on optional equipment and services (insurance, credit offers); 3) both customers and producers still appreciate the personal aspect of sales process, which forms the basis of brand’s presentation and customer loyalty.

https://www.bernsteinresearch.com

Sources of information: ACEA, PwC, McKinsey & Company, ICDP, http://europe.autonews.com, https://www.bernsteinresearch.com